MakerDAO & DAI in Simple Terms

Let’s start with a brief introduction to Decentralized Finance or DeFi as everyone calls it.

Bitcoin was the first blockchain which paved the way for decentralized finance that allowed anyone to receive, send and hold Bitcoin without third party service providers such as banks.

In its current state the Bitcoin blockchain is limited to plain transfers of Bitcoins from one address to another.

Ethereum expanded the idea of blockchain from tracking payments between addresses to all kinds of conditional transfers which opened up ways to hardcode contractual agreements into a blockchain. As a result the concept of Decentralized Finance (DeFi) was born.

The Ethereum blockchain goes far beyond simple transfers and is not limited in complexity of logic that can be coded into a transaction.

Programmers can build any type of public services with complex logic describing the nature of a business or financial contract and let it operate autonomously without means for someone to interfere.

For as long as the Ethereum blockchain is online, these services remain operational, accessible and work exactly as intended.

The term DeFi they usually used as a reference to financial services built on top of Ethereum blockchain or one of its smaller alternatives like EOSIO.

That said, most of the high net worth projects serving the public in the DeFI ecosystem are currently working on top of the Ethereum blockchain.

If you would like to learn more about Ethereum and existing DeFi projects built on top of it, read our Ethereum guide.

1. MakerDAO Overview

MakerDAO is one of the very first DeFi projects built on top of Ethereum blockchain.

The project currently controls worth over half a billion USD, all in an automated manner by a predefined set of rules (aka Smart Contracts) known as Maker Protocol.

Smart Contract is a computer program that lives on a blockchain and transparent in the way it operates. Usually coded in a way it's impossible to change it later.

Anyone with programming skills can locate the smart contract on the blockchain and verify that it works exactly as expected and is without loopholes.

MakerDAO was the first DeFi project to earn global adoption and remains a leader in the amount of funds it controls.

The project launched in 2014 and comes in a form of a Decentralized Autonomous Organization (DAO) which is governed by a geographically distributed set of entities ranging from organizations to private individuals.

MakerDAO operates a lending facility built on the Ethereum where anyone can take out a loan in cryptocurrency in exchange for a small fee.

The governance of the MakerDAO is executed through voting by those in possession of MKR tokens. The incentive for someone to be a part of MakerDAO comes from various public-facing services provided by MakerDAO which drive the value of MKR tokens.

1.1 DAO Explained

If you’re not familiar with the concept of DAO, then simply think of it as a project or organization which meets following criteria:

-

controlled by a distributed group of entities

-

governance exercised through ownership of some token

-

the DAO code operates on an open public blockchain

-

anyone can verify that organization operates as described

-

usually has no official address, office etc

In a way, DAO is an alternative to a traditional corporation where ownership structure is defined by the number of shares someone owns.

Unlike traditional corporations, DAO exists on a blockchain and operates according to pre-coded rules without means for someone to step in and change the rules.

The DAO controlled by entities holding a special token.

If that concept looks somewhat blurry to you then no worries it’s a difficult concept to grasp for someone not familiar with the mechanics of blockchain tech.

At this point you can just take it for granted that such systems have been around for a few years and MakerDAO is one of such systems.

1.2 DAI As A Service

MakerDAO consists of a set of public smart contracts known as Maker Protocol which autonomously handle the lending process.

The DAI cryptocurrency stablecoin is the core product of MakerDAO. It has a fixed value (very close to 1 USD) and is the currency of every single loan Maker Protocol issues to the public.

Most of the services provided by MakerDAO are built around the DAI stablecoin.

The term stablecoin refers to a cryptocurrency which attempts to peg its market value to some external reference, usually it’s USD, EUR or Gold.

The Maker Protocol enables users to lock their Ether tokens as collateral and in return obtain DAI tokens. The collateral released on repayment of the loan and associated service fees.

-

Every time the loan is issued by MakerDAO’s Maker Protocol to someone a new DAI enters circulating supply. At the same time a new collateral in Ether (equivalent to 150% of the DAI loan value) deposited to the Maker Protocol reserves.

-

When the loan returned and associated service fee gets paid, the collateral instantly released back to the user.

-

As the collateral released back to the user the DAI amount retuned by the borrower gets destroyed by the MakerDAO's Maker Protocol.

The Maker Protocol controls the circulating supply of DAI and ensures tha price of DAI remains very close or equal to 1 USD at all times. As will be shown later on the MakerDAO has many tools at its disposal for balancing the price of DAI.

DAI is known as trustless stablecoin because anyone can verify that DAI in circulation indeed backed by a collateral worth 150% of circulating DAI.

That collateral is always there to ensure that every single DAI in circulation can be bought by the MakerDAO smart contracts even if the market demand for DAI goes to zero.

Unlike DAI, most stablecoins (including Tether) are centralized and require a high level of trust from a person holding these coins.

1.3 MakerDAO Governance

Being a DAO the MakerDAO project is entirely governed by anyone in possession of MKR tokens. The ownership of MKR token is directly proportional to the ownership and vote weight on any decision in the MakerDAO.

Ongoing governance of the MakerDAO works through formal proposals which can be voted on and approved by MKR token holders.

- When the proposal meets a certain threshold the code powering the MakerDAO ecosystem gets updated to implement the proposed changes.

- There is no way to bypass this process to implement changes in the Maker Protocol. Only via formal proposals and voting of MKR token holders.

The active proposals can be monitored at https://vote.makerdao.com

Primary MakerDAO services require MKR tokens as payment. As a result, MKR token holders benefit when someone uses MakerDAO services i.e. taking a loan.

MKR token holders financially benefit from the growth of the MakerDAO network. As more people use MakerDAO services the higher is demand for MKR tokens.

At the same time, token holders collectively share the financial risks of DAI stablecoin to ensure its stability, transparency, and efficiency.

Any stability issues with DAI will have a direct impact on the price of MKR token, as the latter will have to be minted (increasing the total supply of MKR tokens) and sold to cover the losses of the Maker Protocol.

At this point, there are slightly over a million of MKR tokens in circulation. The current MKR market cap exceeds half a billion USD.

MKR tokens can be bought and sold on cryptocurrency exchanges just like Bitcoin or Ethereum. The price of the MKR token is determined by the open market forces.

Just like the DAI, the MKR token is an Ethereum based token and can be stored in pretty much any non-custodial wallet.

1.4 Key Players

It should be noted that at the moment there is a key entity in the MakerDAO community known as Maker Foundation. This foundation built and launched the Maker Protocol in conjunction with a number of outside partners.

While the governance of the MakerDAO are exercised through token ownership there are some organizational aspects which are currently overseen by Maker Foundation.

Some of such aspects are the weekly Governance and Risk meetings where the MKR holders talk about the key issues for the present day.

The link here shows the agenda for the past and upcoming meetings. Most of the past meetings are also available on Youtube.

The Maker Foundation is currently working with the MakerDAO community to achieve complete decentralization of the project where all organizational aspects will be managed by the community.

For instance, until recently the Maker Foundation had an exclusive control over the smart contract that controlled the operational mechanics of the MKR token. While any changes to that smart contract can't go unnoticed, the Maker Foundation been privileged in ability to control it.

In March 2020, the control of that contract passed to the MakerDAO community. You can read more about this here. There are means to verify that this change actually took place by exploring the relevant transaction on Ethereum blockchain itself.

There is also an entity known as DAI foundation which was formed to oversee and legally control MakerDAO's key intangible assets, such as trademarks and code copyrights.

It's based in Denmark and operates solely on the basis of objective and rigid statutes that define its mandate.

2. MakerDAO Services

As briefly mentioned earlier the DAI cryptocurrency is the core product of MakerDAO. The public facing services provided by MakerDAO are built around the DAI stablecoin.

MakerDAO provides following services:

- Oasis: decentralized cryptocurrency exchange

- Ability to take a loan in DAI from Maker Protocol

- Ability to lend DAI to Maker Protocol and earn interest

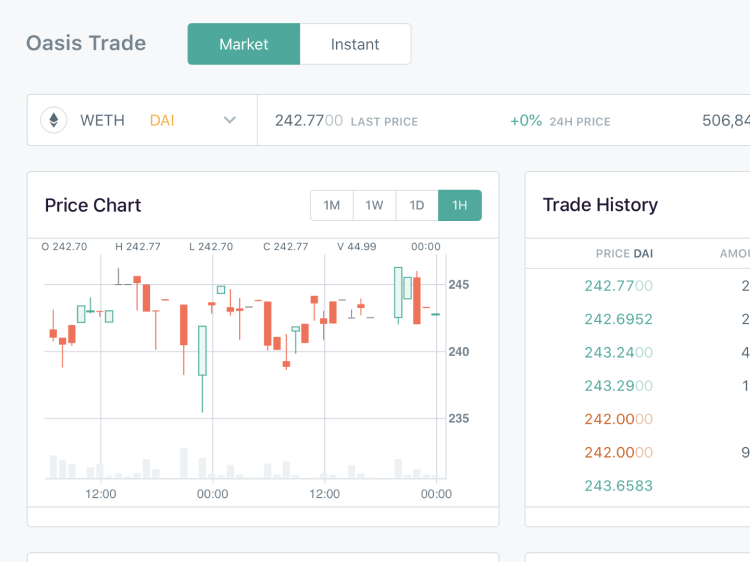

2.1 Oasis Exchange

The Oasis is peer-to-peer (decentralized) platform where anyone can exchange Ethereum and Ethereum based tokens including DAI.

Being a decentralized platform, the service operates fully on Ethereum blockchain. It is open to all and free to use except for the actual Ethereum transaction fees for exchanging tokens.

While the Oasis platform is accessible through a website, the services it provides can be also accessed by communicating with the Ethereum blockchain directly.

The Oasis website is just one of the many ways to interact with the Maker Protocol.

Those familiar with programming on Ethereum can access MakerDAO services by interacting with Maker Protocol smart contracts using various means and not use the website at all.

To deposit or withdraw funds from the Oasis website user needs one of the supported Ethereum wallets like Metamask wallet built for Google Chrome.

Keep in mind when you interact with decentralized platforms like Oasis token exchange there are no means to roll back anything if you make a mistake with funds somewhere. All transactions are final and irreversible.

Oasis also provides means to access core MakerDAO services such as borrowing and lending DAI tokens.

2.2 Borrowing DAI

One of the core services provided by MakerDAO is the ability to borrow DAI tokens from the Maker Protocol in exchange for locking Ether tokens as collateral.

Currently, the Maker Protocol accepts Ether and some Ethereum-based tokens:

- ETH : Ethereum token

- BAT : Basic Attention Token

- wBTC : wrapped Bitcoin

- USDC : stablecoin from Coinbase

The list of accepted tokens that can be used as collateral as well as individual requirements for each collateral type can change when the MakerDAO governance decides to do so.

The borrowing steps:

-

The user starts with sending Ethereum or other supported token as collateral to a smart contract known as Maker Vault.

-

Maker Vault smart contract locks in the received Ether and in exchange allows the user to generate a certain amount of DAI tokens, depending on the current market price of the Ether.

-

Maker Vaults operate offer fairly flexible terms. There are no repayment schedules and no credit history requirements. Users can repay at their own pace as long as their Vault is properly collateralized.

Users interact with Maker Vaults and the Maker Protocol directly. The user has complete and independent control over their deposited collateral as long the real-time value of collateral doesn’t fall below the required minimum level.

The Maker Vault is a core component of the Maker Protocol, which facilitates the generation of DAI against locked up collateral.

All DAI in circulation are created by Maker Vaults and more importantly have underlying assets backing each DAI.

Each user borrowing DAI generates a unique Maker Vault as a result of that action.

-

Collateral Type

Depending on the collateral asset the generated Maker Vault will have some custom collateral-based attributes.

-

Collateralization Ratio

Maker Vaults require a collateral 150% worth of the requested DAI amount. In other words, to borrow 100 DAI you will need to lock 150$ worth of Ether tokens as collateral.

The 150% requirement for Ether collateral may change if the MakerDAO decides to do that. The ratio of 150% currently applies when user uses Ether as s collateral. For other tokens the value may be different.

-

Vault Health

As the price of the collateral assets fluctuate the collateralization ratio for each vault changes along with it, in real time. The 150% is a minimum requirement for the vault to remain operational.

When the price of Ether increases so is the collateralization ratio of each vault, allowing users to generate even more DAI from those vaults without the need to add any more collateral.

The reverse is true as well, if the price of Ether goes down significantly the vault can become under collateralized and be at risk of liquidating.

When the collateralization ratio of the Vault nears 150$ the user may either deposit more collateral into it or return a portion of the borrowed DAI.

It’s a responsibility of the user to regularly monitor the vault and ensure it remains healthy.

-

Liquidation

The vault is considered healthy when it’s collateralization ratio is above 150%. Liquidation is the process that is automatically initiated by the Maker Protocol when the collateralization ratio of the vault falls below 150%.

During the liquidation process the collateral automatically auctioned on the market with an aim to buy the amount of DAI the vault has issued to the user.

During the Liquidation process, enough collateral is sold to cover the debt along with a liquidation penalty (equivalent to 13% of collateral). Whatever remains will be returned to the user.

-

Stability Fee

To reclaim the collateral in the Vault, users must repay the borrowed amount of DAI, and the accumulated stability fees.

Stability fee paid by every vault owner and can be calculated based on annual percentage yield of 0.5%. Stability Fees must be paid in DAI or MKR token.

As will be explained below, Stability Fee is one of the mechanisms of MakerDAO to control the price of DAI and maintain the 1-1 USD peg.

Just like the other aspect of the Maker Protocol, the stability fee amount can change as a result of voting by MKR token holders.

2.3 Lending DAI

In November 2019 the MakerDAO project received a major upgrade. The upgrade introduced the capability for users to deposit DAI holdings to Maker Protocol and earn an interest rate known as DAI Savings Rate (DSR).

The user sends DAI tokens to a smart contract which keeps the funds locked and tracks the accrued interest rate just like a regular savings account that pays an interest on your savings. There are no withdrawal limits, deposit limits, or liquidity constraints.

The Maker Protocol pays depositors an interest rate from the funds it accumulates from Stability Fees collected as a result of borrowing by public.

Since the Maker Protocol pays the DSR from funds earned through Stability Fee – the DSR can never exceed the Stability Fee. If the current Stability Fee is 0.5% then the DSR can't exceed that amount.

The list below shows how the DSR rates have changed over time:

- Nov 2019 : 2.00 %

- Dec 2019 : 4.00 %

- Jan 2020 : 6.00 % (Jan 8'th)

- Jan 2020 : 7.75 % (Jan 26'th)

- Feb 2020 : 8.75 % (Feb 4'th)

- Feb 2020 : 7.50 % (Feb 9'th)

- Feb 2020 : 8.00 % (Feb 20'th)

- Mar 2020 : 4.00 % (Mar 15'th)

- Mar 2020 : 0.00 % (Mar 17'th)

On March 17’th, MakerDAO dropped the DSR to 0% with an aim to bring the value of DAI closer to 1$. The reason for this will be explained below.

Just like the Stability Fee rate, the DAI Savings Rate (DSR) amount is decided by the MakerDAO vote.

3. DAI Stability

MakerDAO has been able to consistently sustain the price of its DAI token in the close range of 1$ over the last couple of years.

With active borrowing and lending mechanisms in place, the DAI can be considered a fairly robust stablecoin. Merchants worldwide both online and offline can potentially consider accepting it as a means of payment.

Someone can sell the merchandise for DAI and then deposit received DAI to Maker Protocol and earn an interest rate.

Both Stability Fee and DAI Savings Rate, provide MakerDAO with the practical means to control the supply and demand side of the DAI stablecoin.

3.1 DAI Price

Let’s see how MakerDAO can keep the price of DAI token at $1 via supply and demand controlling mechanisms at its disposal.

To increase the price of DAI:

-

Let’s assume the DAI price on the market fell to 0.99$ and the MakerDAO needs to bring it back to 1$. To address this the MakerDAO may increase the demand (or reduce supply) for DAI tokens.

-

The demand for DAI can be boosted by increasing DSR. The higher DSR the more people will try to deposit DAI holdings into Maker Protocol and earn interest.

-

At the same time, the increase in Stability Fees can make it more expensive to create new DAI and prevent the supply from increasing supply.

To decrease the price of DAI:

-

Now, let’s say that at some point the price of DAI went to 1.01$. At this point the MakerDAO needs to reduce the price, bringing it closer to 1$. To address this MakerDAO may reduce the demand (or increase the supply) for DAI tokens.

-

The decrease in DSR is likely to reduce the demand for DAI tokens as fewer people would want to deposit DAI holdings and earn interest.

-

At the same time, the Stability Fees can be brought down further and make it cheaper to create new DAI and increase the circulating supply. This in turn should push the market price of DAI lower.

In the next section we'll look at what happens when the price of the collateral assets like Ether falls sharply.

3.2 DAI vs MKR

The Maker Protocol is what controls the number of DAI circulation. It also ensures that DAI in circulation backed by a collateral valued at least 100% of the amount in circulation. The 150% collateral requirement for generating new DAI ensures there is a significant cushion for the Maker Protocol.

That said, there is always a chance for the price of collateral assets to change so quickly that the cumulative value of the underlying collateral can fall short of DAI in circulation.

-

Should the price drop of collateral be significant enough to cause a shortfall in collateral relative to DAI borrowed, the MakerDAO can mint new MKR tokens.

-

Those newly minted MKR tokens then auctioned for DAI. The bought DAI then destroyed. This action normalizes the system by reducing the DAI in circulation while keeping the collateral assets same.

Such setup encourages the MKR tokwn holders to govern the MakerDAO system well and charge an appropriate Stability Fees for the loans they are insuring.

If the MakerDAO governors issue bad debt, it is the Maker governors (MKR token holders) who pay.

The cost comes in a form of new MKR tokens entering circulation and diluting the value for the MKR token holders.

If for some reason the value of the MKR token gets wiped out, then DAI holders would ultimately suffer, but there is no situation where MKR holders are bailed out at the expense of DAI holders.

The recent issue in the MakerDAO is an ideal example to illustrate this in action. There used to be exactly 1,000,000 tokens right until March 2020. In mid March 2020 there was an incident as a result of which MakerDAO ended up with about 4.5 million worth of bad debt.

-

Due to a series of unforeseen events the Maker Protocol failed to liquidate some collateral held in a number of Maker Vaults when the collateralization ratio in these vaults fell below 150%.

-

This happened on the day when Ethereum price dropped nearly 50% in a single day, the biggest daily drop in its history.

-

That drop caused massive activity on the Ethereum blockchain as a result of which the automated liquidation process did not execute as it was supposed to.

Long story short, about 4.5 million worth of DAI that should have been destroyed by Maker Protocol didn’t get destroyed. To account for that, MakerDAO initiated a so called Debt Auction where new MKR tokens were printed and sold for DAI and then destroyed by the Maker Protocol.

3.3 The Maker (MKR) Price

As was shown earlier, the MKR token holders govern the MakerDAO and the Maker Protocol via voting. The value of the MKR token comes from the ability to control the MakerDAO protocol and its various aspects.

-

When the MakerDAO is governed well the amount of MKR in circulation can be potentially decreased and push the value of the remaining MKR tokens higher.

-

In the same way, poor governance may result in the dilution of the token value. This is primarily due to the fact that MKR token holders will ultimately have to cover the losses of the Maker Protocol (if there are any).

As more people start to use MakerDAO services the demand for the MKR tokens should keep rising. The fees collected by MakerDAO can potentially be used to buy the MKR tokens from the market and then destroy them, thereby reducing the MKR token supply.

The page here shows how the market price of MKR token has changed over the last few years.

Conclusion

To this day, MakerDAO is widely considered as one of the most successful Decentralized Finance projects as well as one of the very first projects that operate under the DAO model.

For many the project has proved that DAO governance model is a viable one. The beauty of such a model is that it doesn’t discriminate and allows pretty much anyone to take part in the governance of the project.

Those who invested in MakerDAO in early stages saw significant return on their investments. However, it’s yet to be seen whether the project will be able to handle unforeseen events in the future and survive.

There are many uncertainties which may result in significant risks for the project ranging from the undiscovered software bugs in the code powering MakerDAO smart contracts to the potential issues in the Ethereum blockchain itself.

Done! Check your email.

Done! Check your email.